Casual Info About How To Build A Swap Curve

Yield Curve Building In Excel Using Swap Rates - Resources

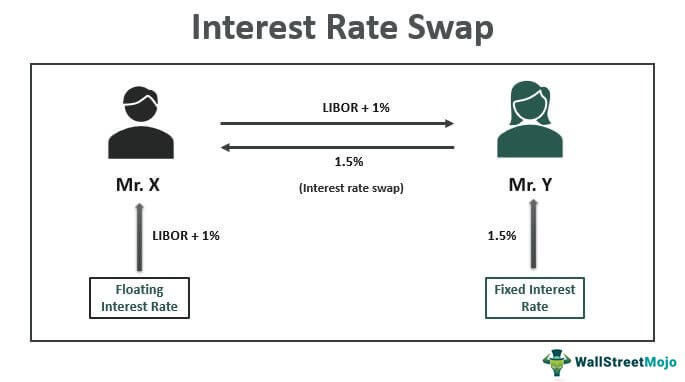

Interest Rate Swap | Examples Uses Curve Wsm

Modeling And Forecasting Interest Rate Swap Spreads

Perfect Bloomberg Price Match Of An Interest Rate Swap In Excel By Using Dual Bootstrapping - Resources

2

Modeling & Stressing The Interest Rates Swap Curve | Moody's Analytics

V abstract the swap market has enjoyed tremendous growth in the last decade.

How to build a swap curve. Notice, yield curve inversion in the front of the. Build, visualize, and analyze the swap curve. The table at the bottom supplies the swap rates and consists of two columns.

Vanilla irs, where one party pays a fixed coupon. Curve building for a swap. A swap curve is the name given to the swap's equivalent of a yield curve.

I need some help to figure out the mechanics in building the long end of a swap curve, i have followed a example on how to do it, see this link [url removed, login to view] i need help to finish. Modified 2 years, 8 months ago. Bootstrapping method is used to extract.

Our white paper, swap curve building at factset: Prior to the gfc, a single yield curve was the output of the process of curve construction. The short end of the forward curve (up to two years) is constructed using sofr future contracts (a liquid futures market reflecting the anticipated sofr on the settlement.

A swap curve identifies the relationship between swap rates at varying maturities. A swap curve is constructed with deposits in the short end until 3m, ir futures in the middle until 2y, and with par swaps until 30 to 50y in the long end. F fe +θ=θ(6) in building the curve in the futures region, formula (4), along with the compounding conversion (6), is applied to each futures period independently, and piecewise forward rates.

The pair ibor index= %gbplibor|6m supplies the conventions of the floating leg index. With government issues shrinking in supply and increased price volatilities, the swap term structure has emerged.

2

Multiple Curves, Pricing Interest Rate Swap With Collateral

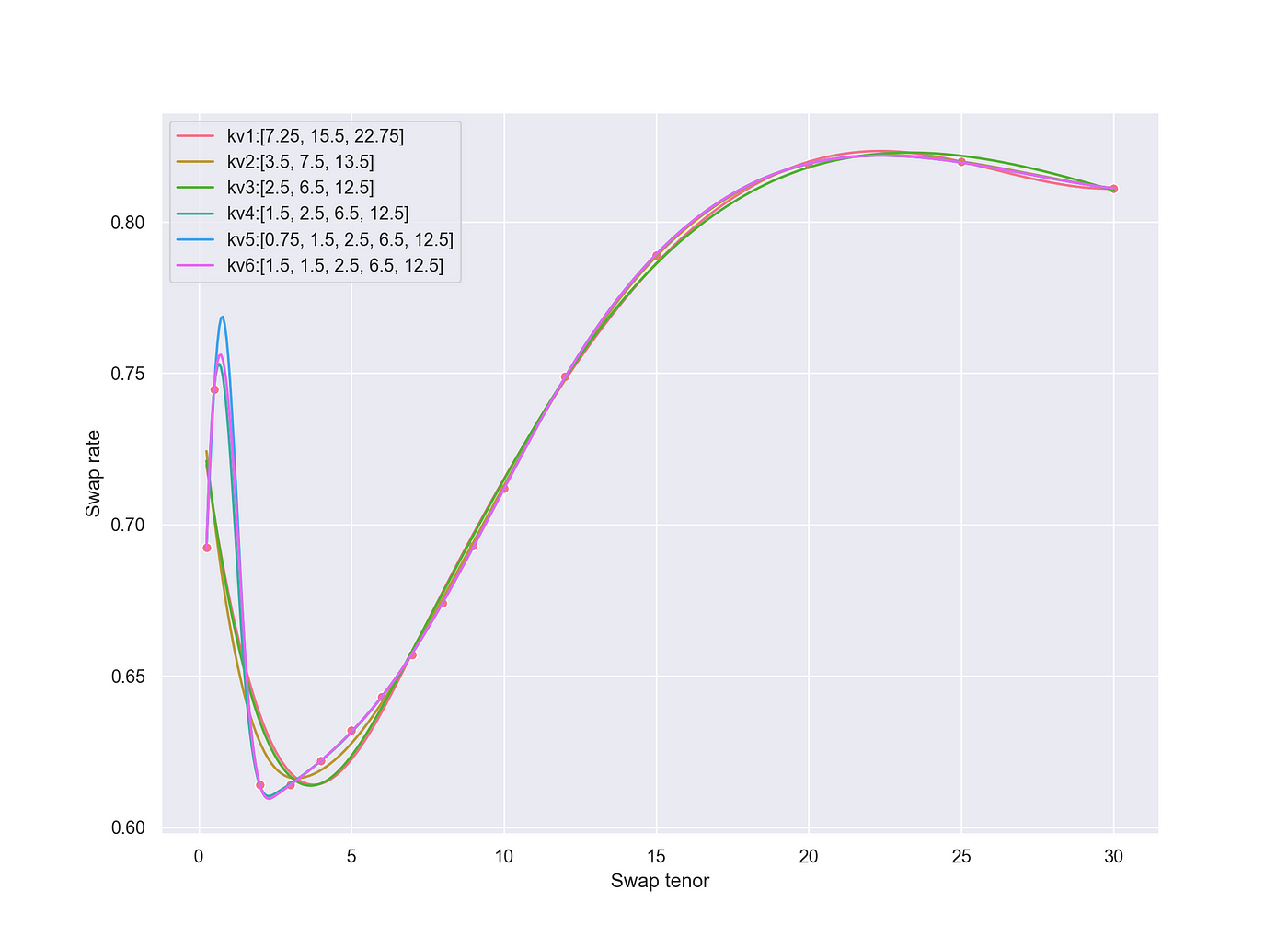

Yield Curve Building In Python. Using Swap Rates & B-spline Functions… | By Neil Chandarana Towards Data Science

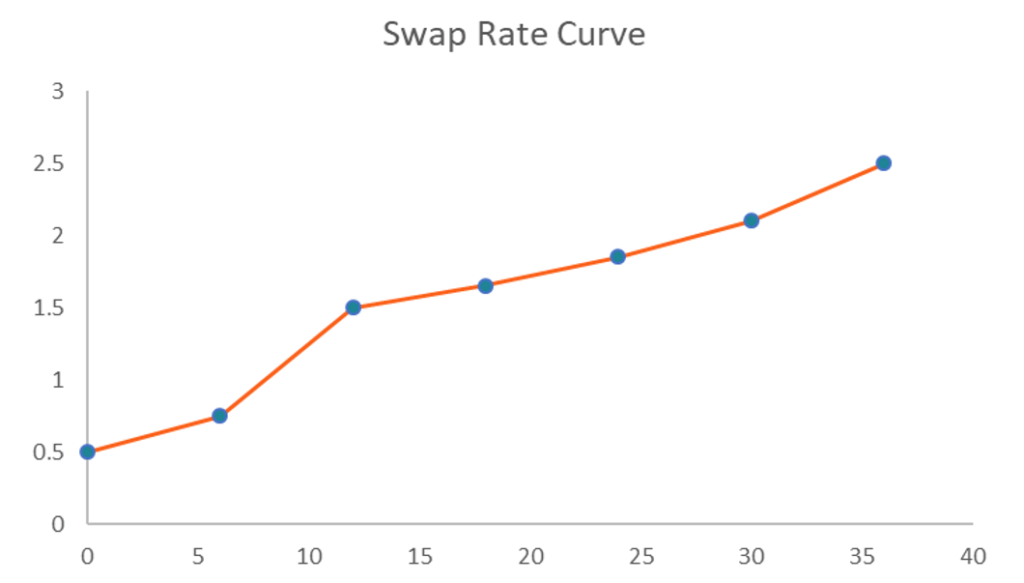

Swap Rate Curve - Overview, How To Create In Excel

Interest Rate Swap | Examples Uses Curve Wsm

/dotdash_Final_How_to_Value_Interest_Rate_Swaps_Sep_2020-01-4b6f55263e5a41b091bded09d63da811.jpg)

How To Value Interest Rate Swaps

Revisiting "the Art And Science Of Curve Building" | Fincad

2

Yield Curve Building In Python. Using Swap Rates & B-spline Functions… | By Neil Chandarana Towards Data Science

Vandever Capital | Blog

:max_bytes(150000):strip_icc()/dotdash_Final_How_to_Value_Interest_Rate_Swaps_Sep_2020-05-ebe661886e084d879c91c96ab4cbf63b.jpg)

How To Value Interest Rate Swaps

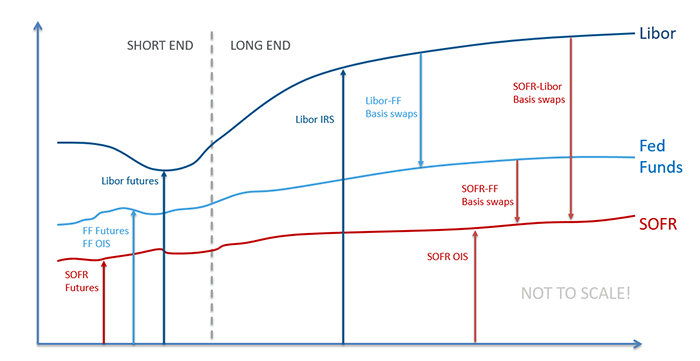

Connecting The Sofr Curve To Swaps | Fincad

A List Of Instruments Used To Build Usd Interest Rate Curve This... | Download Scientific Diagram